| Home | > | Software | > | Stock Models | > | Binomial Model | > | Binomial

Model Demo |

Forfeiture & Expected Life Tool Public Company Volatility Service

Download our Whitepaper (494KB)

|

Overview

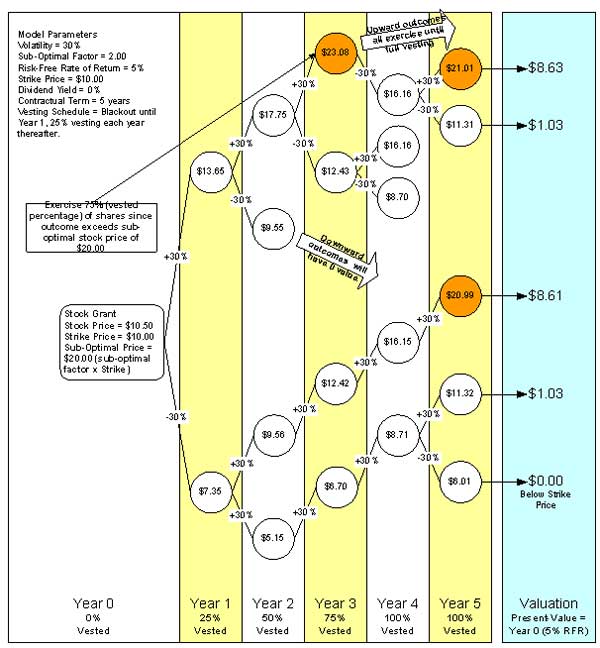

Current Accounting Standards Codification, ASC 718 (formerly FAS123r) requires that companies that issue stock-based payments must now determine a valuation and record these options in their financial statements. Several solutions are available to meet this requirement including the venerable Black-Scholes model. Newer models exist including the powerful Binomial Lattice model as described in this demo (see the model comparison for a summarization of the key features of each model). The Binomial Lattice model produces a wide set of possible stock price and option exercise possibilities that are averaged together to produce a per-option value based on all of the scenarios and an 'implied life' that indicates the likely life the option could be expected to remain unexercised. See Figure 1 for a graphical depiction of the Binomial Lattice computation.

Figure 1. Binomial Lattice models consider stock price changes over time based on inputs such as Expected Volatility and Expected Dividend Yield to create a set of computed stock price/option exercise outcomes. Our model takes inputs from the 'Option Assumptions' sheet and uses this information to produce the output valuation and a variety of important statistics on the model output. If any inputs are out of range, an error will appear indicating the source of the error and the expected range. |

|

Financial Reporting Solutions

©2004,

2005. ProCognis, Inc. All Rights ReservMay 24, 2011008

Service

Agreement & Privacy Policy